Employee Ownership Trusts in Canada

Reading Time: 4.5 minutes

More than just offering significant tax incentives, an Employee-Owned Trust (EOT) keeps ownership within the organization, selling to those who helped build it— the employees—who then maintain the owner’s and organization’s values and legacy.

Usually, the alternative is selling to a private equity firm or foreign buyer that may take the company in a different direction, not considering the people and/or values that got it to where it is today.

Employee ownership has a long track record of being good for succession, employees, companies, and communities. As a result, the UK and the US provide significant tax incentives for business owners who sell to the workers. Canada is now following suit, exempting the first $10M of capital gains from income tax for sales to EOTs. This exemption is only available until the end of 2026.

How Selling to an Employee-Owned Trust (EOT) Works

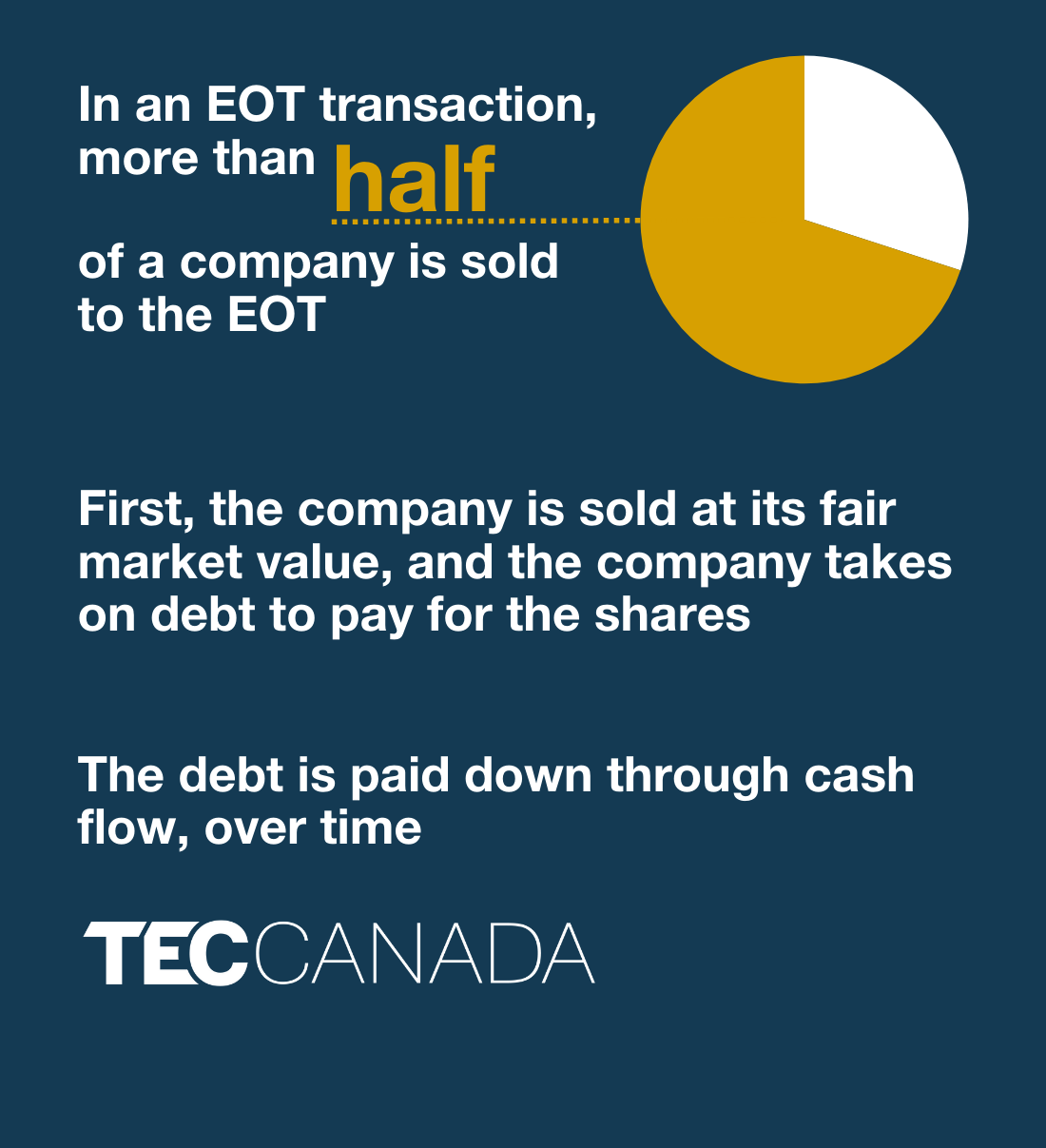

In an Employee-Owned Trust (EOT) transaction, more than half of a company is sold to the EOT. The EOT will then hold shares and become the owner on behalf of all its employees. First, the company is sold at its fair market value, and the company takes on debt to pay for the shares. The debt is then paid down through cash flow, over time.

In an Employee-Owned Trust (EOT) transaction, more than half of a company is sold to the EOT. The EOT will then hold shares and become the owner on behalf of all its employees. First, the company is sold at its fair market value, and the company takes on debt to pay for the shares. The debt is then paid down through cash flow, over time.

This way, employees don’t need to have money to facilitate the transaction and the benefits can be shared among them. That broad sharing of benefits is what provides some of the rationale for governments to provide tax incentives.

For example, the company’s shares will be sold to the EOT, and the owner provides a vendor take-back loan to pay for the shares. Then, the company pays out the owner out of cash flow over what’s typically a 5 to 10-year period until the full value of the shares have been paid. Depending on the company, a bank may loan some of the purchase price so the seller can receive some cash on exit.

Did you know…?

With 75% of small business owners in Canada planning to exit their business within the next decade, the new employee ownership trust (EOT) rules offer a fresh opportunity for succession planning.

Source: CFIB’s national survey of business owners between June and August 2022

How the Tax Incentive Works

The government wants to encourage these transactions because they keep businesses local and involved with their communities. Employee-owned companies also tend to grow faster and are more resilient and productive than those sold to a third party. They have great wealth-generating benefits for workers. However, business owners are taking on additional risk in selling to an EOT and will get paid over a longer period than in a traditional sale. That’s where the tax incentive comes in.

Owners of private Canadian companies can qualify for up to $10M in tax-free capital gains in a sale to an EOT. The $10M is to be divided amongst the sellers in whatever way they choose.

Only individuals qualify, so a company selling a division to its workers would not qualify. Only owners who’ve been active in the company can take advantage of the incentive – you have to have worked for at least two years in the business at some point in the past. The incentive isn’t designed for passive investors in the company.

There are other qualification rules to discuss with your advisor, but most owners of Canadian companies should qualify for the incentive. Importantly, the EOT tax incentive does not affect your ability to use the Lifetime Capital Gains Exemption (LCGE) – the EOT incentive can be used in addition to the LCGE.

Running the Company After the Sale

While the EOT owns the majority of the company shares, it doesn’t operate the company day-to-day. This is sometimes referred to as “indirect employee ownership,” where the employees receive the financial benefit of the company without directly making decisions. That falls to the business leaders and management team, who will report to a board of directors. If the business owner selling the company is the CEO before the sale, they can remain the CEO after the sale if they choose.

The EOT will have a trustee or a Board of Trustees to make decisions on behalf of the employee shareholders. At least one-third of the trustee Board needs to be employees of the company. So, it could be a single-employee trustee, but will more commonly have multiple people, for example, a five-person Board of trustees with two employees.

Beneficiaries of the EOT

If the company has enough cash to distribute dividends, or if it is purchased, the money is given to employees based on the EOT’s ownership percentage.

A formula established in the EOT agreement decides how the money gets divided. The business owners and the Board of Trustees will jointly decide the formula. It might distribute benefits based on one or a combination of three factors: salary, hours worked, and tenure at the company. There can also be distinct formulas for different scenarios, such as an annual dividend disbursement or a company sale.

For instance, a person earning $50K annually would receive half the yearly profit share of an individual earning $100K. However, if the company is sold and the $50K earner has a tenure of 30 years, they might receive a significantly larger share than a $100K earner who has just joined the company.

The Canadian EOT is very flexible, and each owner should consider the best approach for their company and employees.

Good Candidates for Employee Ownership

Business owners who sell to EOTs are generally passionate about their companies, communities, and employees’ development. They are often against selling to the most common buyers, like competitors in their industry or private equity companies. They want to preserve the company culture they’ve worked years to build and the jobs in their local communities. A lot of Canadian business leaders feel this way, as shown in this survey of business owners by the Canadian Federation of Independent Business.

There are industries and sizes where EOT sales tend to be more popular, but all types and sizes of businesses can benefit. Common industries are construction, wholesale distribution, light manufacturing, retail, finance, IT consulting, and professional services.

Most companies have between 25 and 250 employees when they sell, with a tiny minority larger than 1,000. Businesses smaller than 25 employees may not have the administrative capacity to manage an EOT structure. There aren’t many privately held companies that are bigger than a few hundred employees.

The best candidates for EOTs are companies with strong and consistent cash flows in mature industries with a thoughtful management transition either in place or in progress. This lowers the risk of the transaction and helps ensure that there’s sufficient cash to pay the purchase price of the company, leaving a lot of the future benefits left over for a company’s employees.

The Next Step

Talk to an advisor! Many details couldn’t be covered here, and a successful transition will take a lot of planning. Secondly, consider joining a peer advisory group of effective leaders or a leadership development program. Having a sounding board while making major decisions like selling to an Employee Ownership Trust is beneficial for all leadership styles.